GoldenBee Research on CSR Reporting in China 2021 Released

2021-12-31GoldenBeeGoldenBee0

As the opening year of Chin's 14th Five-Year Plan (2021-2025), 2021 has ushered in a new stage of China's economic development. At this significant and historical time, Chinese companies have shown their dynamic motivation for process and good. This is a positive signal found in the GoldenBee Index on Corporate Social Responsibility Reporting in China 2021 ("the Index Report" for short).

Based on GoldenBee CSR Report Assessment System 2021 (GBEE-CRAS2021), 1,802 Chinese CSR reports released by companies in China from January 1 to October 31, 2021 are collected and assessed in this Index Report, the 13th CSR Index Report released by the GoldenBee Research Team.

According to Guan Zhuxun, Executive Vice President and Chief Operating Officer of GoldenBee Consulting, the GoldenBee "Three Excellence" theoretical model of CSR reporting, namely excellent basic information disclosure, excellent response to core content, and excellent compliance with basic principles, was applied in the Index Report. GoldenBee profoundly analyzed the characteristics of CSR reports released in China, and offered suggestions on the CSR reporting in China to provide reference for enterprises.

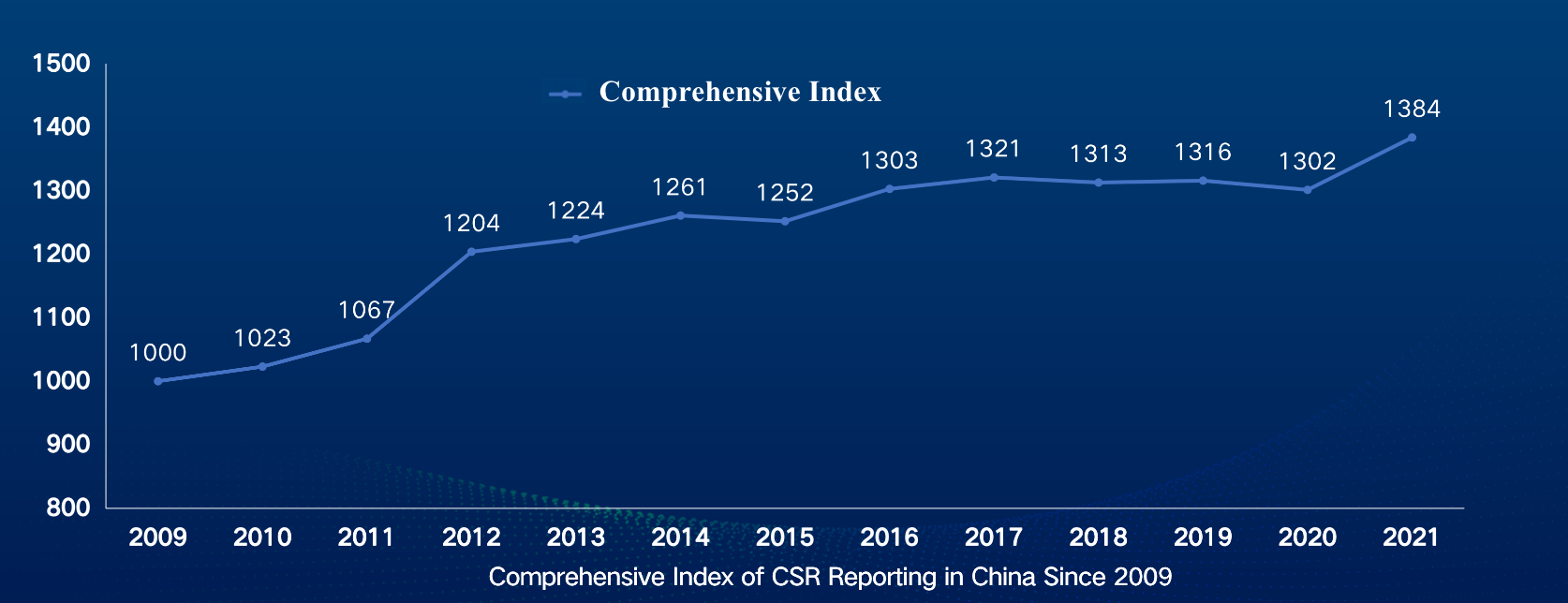

Characteristics 1:In 2021, the report quality reached an all-time high, and the comprehensive index reached 1,384 points, with a year-on-year increase of 6%. The proportion of reports in the development, good, and excellent stages increased year on year, the proportion of reports in the catch-up stage increased greatly, and those in the starting stage have decreased significantly. It is predicted that China's CSR report quality will advance to new levels during the 14th Five-year Plan period.

Characteristics 2: The information disclosed in the reports is generally objective and true, focusing on comparability and innovation. The index of six report dimensions has been improved year on year: improvement of credibility shows that the overall information disclosure is objective and impartial, disclosure of negative information has been strengthened; and improvement of comparability reflects that the CSR index management has been enhanced.

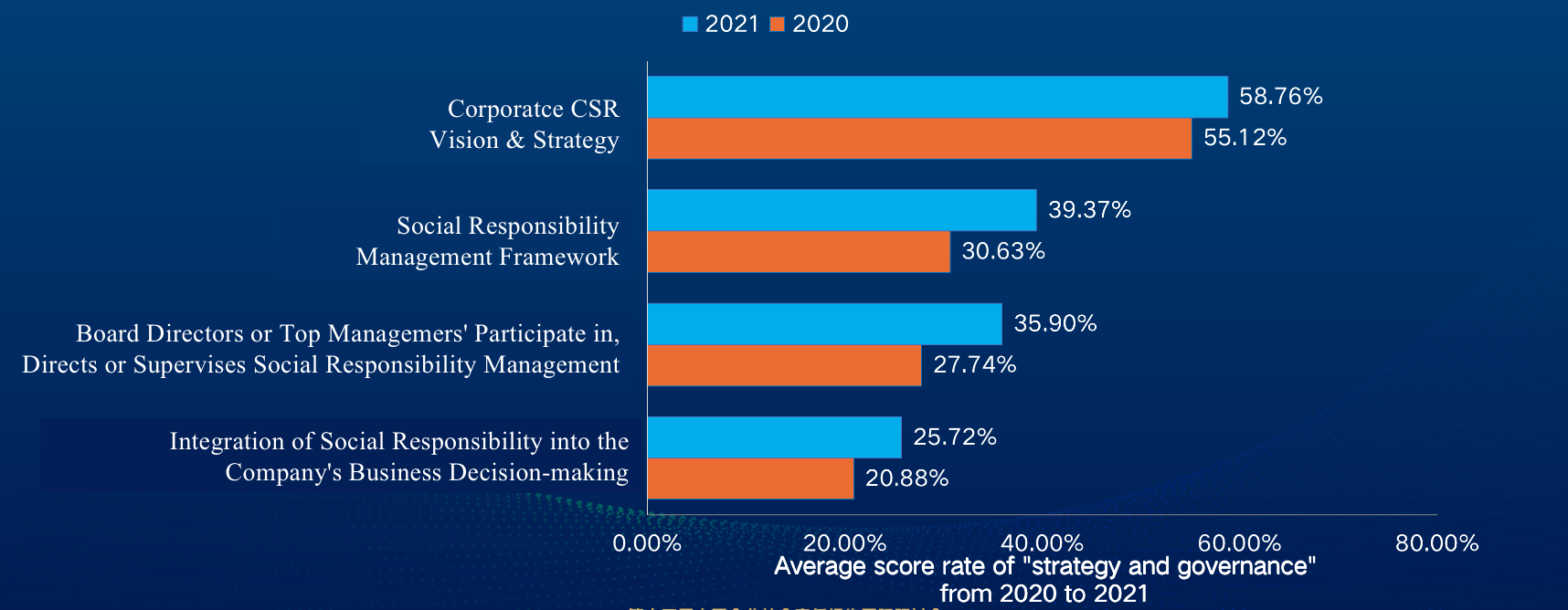

Characteristics 3: The disclosure on corporate strategy and governance has seen a significant improvement, and information about top leadership's participation in social responsibility management has greatly increased. This year, the disclosure rate of different indicators of corporate strategy and governance has increased significantly year on year. Nearly 60% of the companies disclosed their CSR vision and strategy in their reports, and about 40% of them disclosed their social responsibility management framework in the reports.

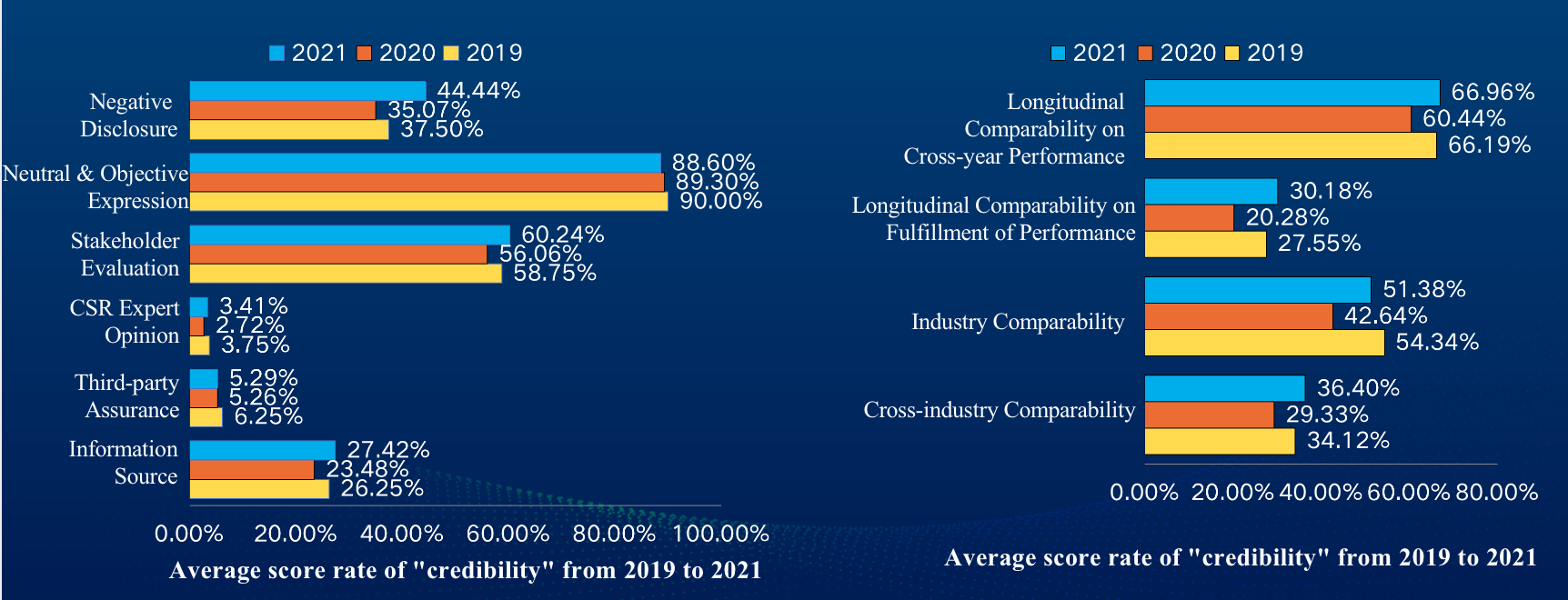

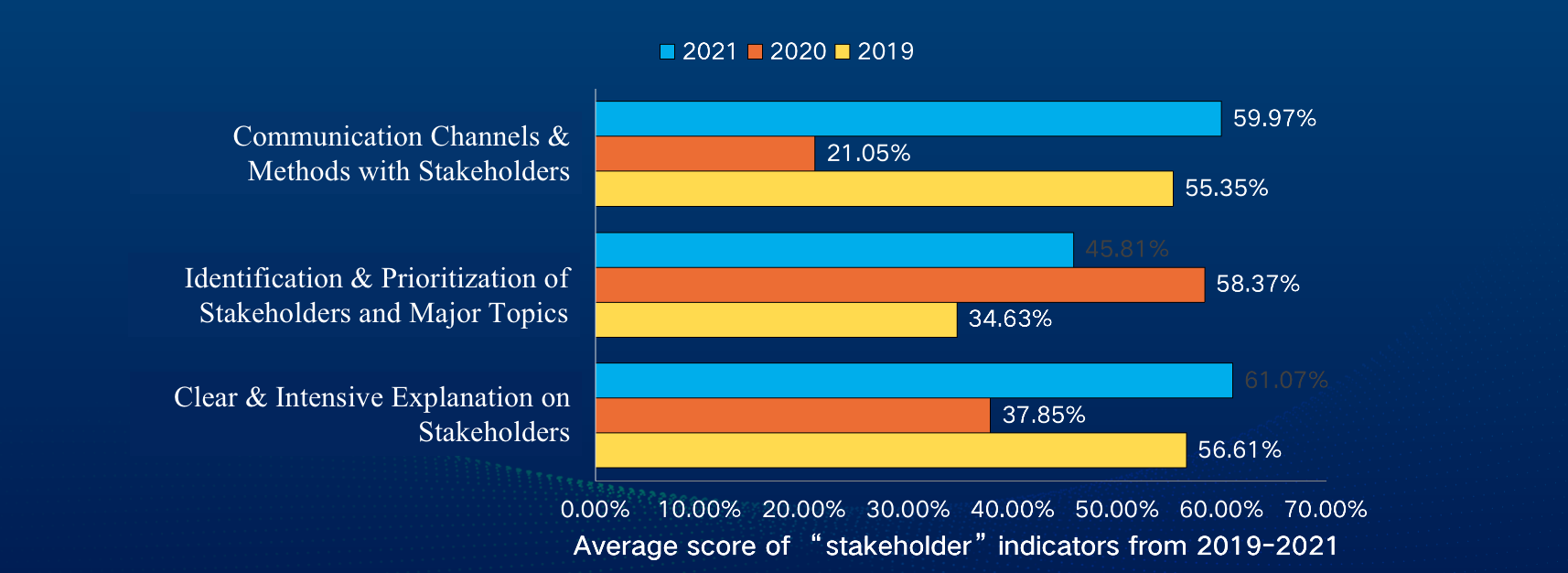

Characteristics 4: The reports focus more on the performance of responsibilities to stakeholders, seeing a rising response to the expectations and demands of stakeholders. In 2021, the score rate of reports on the "communication channels and methods with stakeholders" and "clear and intensive explanation on stakeholders have increased significantly year on year, reaching nearly 60% respectively. A deeper analysis revealed that the information disclosure of key stakeholders such as employees, communities, customers, environment, and suppliers has expanded from CSR practices to the CSR concepts, requirements and expectations, communication channels and methods, and performance disclosures.

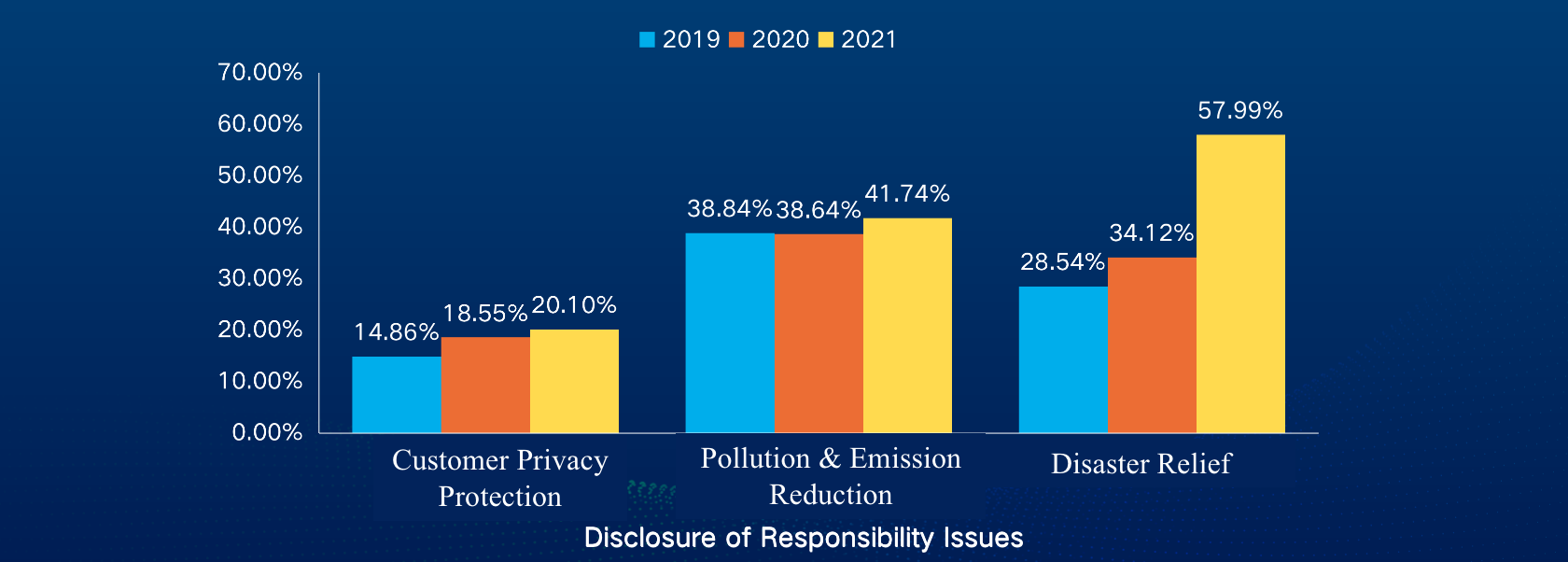

Characteristics 5: The reports disclose more information on fulfillment of responsibility to stakeholders, such as customers, environment, suppliers, communities, with higher disclosure rate of key topics such as customer privacy protection, pollution reduction and emission reduction, procurement principles, community voluntary activities, donation and disaster relief.

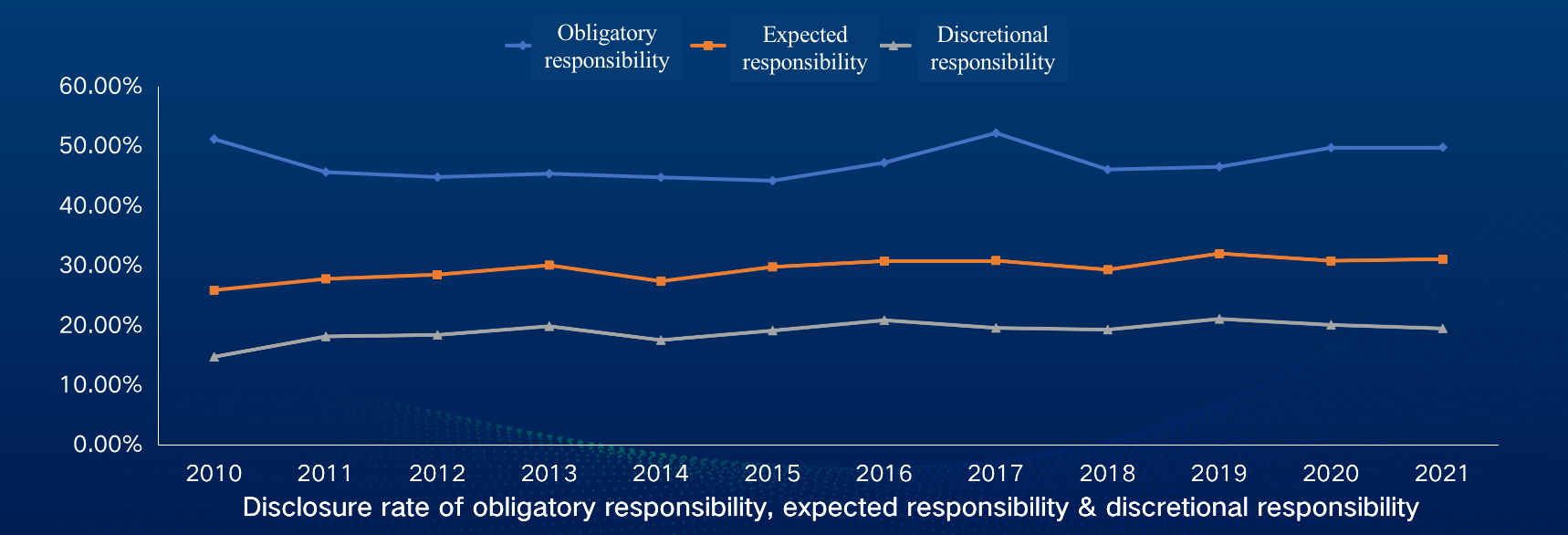

Characteristics 6: The data is consistent with the stage of China's CSR development, which indicates that corporate information disclosure is more pragmatic. The indicator disclosure rates of the obligatory responsibility, expected responsibility and discretional responsibility are 50%, 30% and 20% respectively.

Characteristics 7: The quality of reports in financial and insurance industry and information technology industry has improved significantly. The index of production and supply industries of electricity, coal, water and gas has always been at a high level, and the report quality of transportation, warehousing and real estate industries has decreased. In 2021, the report quality of the social service industry has surpassed the transportation and warehousing industries, becoming the best for the first time. Compared with the base period, the index of ICT industry increased by 60.01%; the index of the financial and insurance industries has continuously improved for three years, seeing an increase of 23.87%; the index of production and supply industries of electricity, coal, water and gas increased by 31.59%.

Characteristics 8: The gap between the report quality of enterprises of different ownership has been further narrowed. The report quality of state-owned holding enterprises and private enterprises has increased significantly year on year. In the past three years, the quality of reports from central SOEs has always maintained at a relatively high level, which is much higher than that of other types of enterprises.

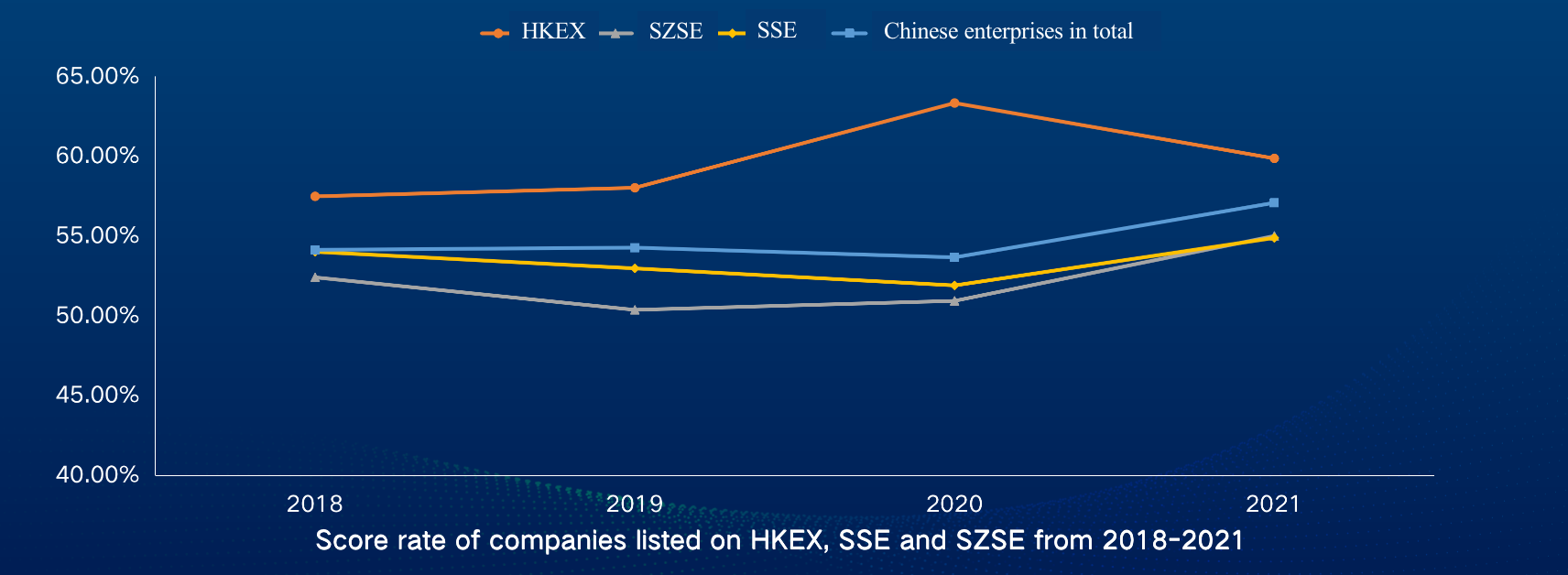

Characteristics 9: The report quality of mainland companies listed on SSE and SZSE has significantly improved year on year, and the gap between the report quality of mainland companies listed on SSE and SZSE and that listed in Hong Kong has narrowed. Since 2018, the mandatory implementation of the ESG Reporting Guide of the HKEX has promoted the report quality of mainland companies listed on the HKEX.

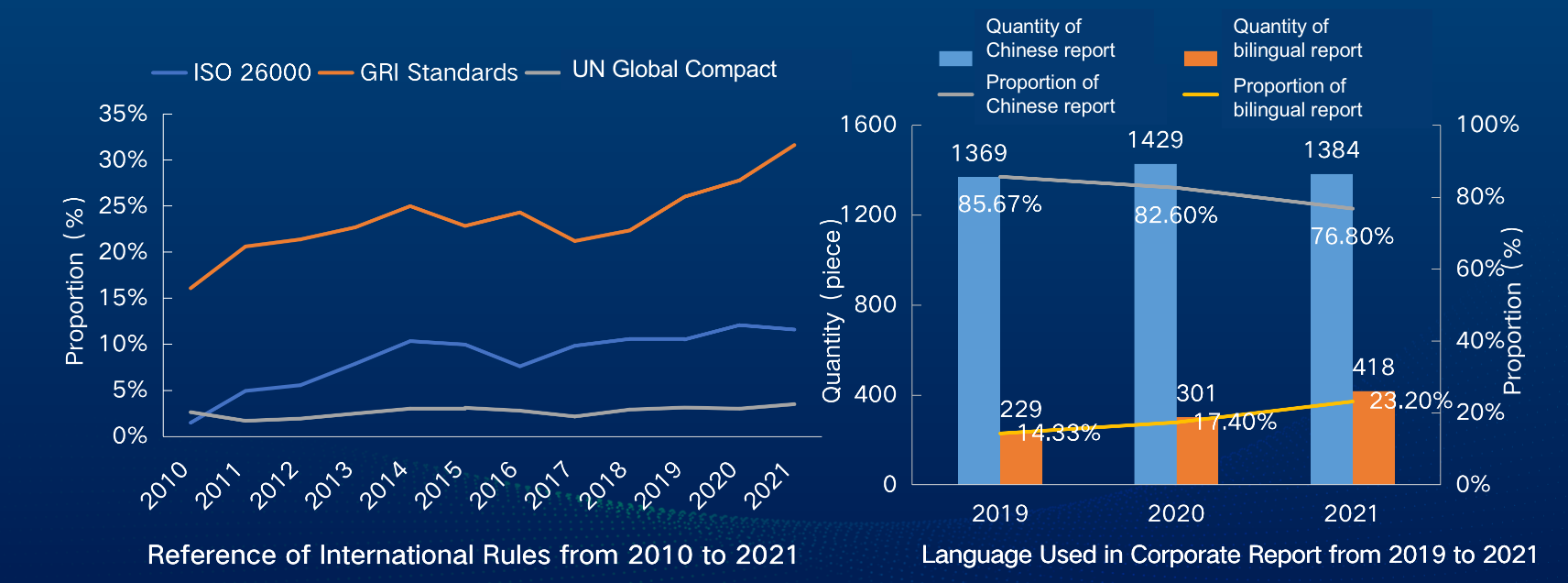

Characteristics 10: The number of reports prepared in accordance with international standards and bilingual reports has increased rapidly. In 2021, reports prepared in accordance with GRI Standards have increased by 5.61 percentage points year on year. Reports that refer to ISO 26000 and the United Nations Global Compact have also increased slightly.

Suggestion 1: Seize the opportunities and momentum to strengthen the understanding and action that make social responsibility help enterprises develop with high quality, and promote the quality of CSR report to a new level during the 14th Five-year Plan period.

Suggestion 2: Guided by strategies and the concept of stakeholders, to strengthen the disclosure of CSR strategy, governance and management.

Suggestion 3: Be problem-oriented and focus on the expectations and demands of stakeholders, making up for the shortcomings of reports in normality and materiality, and giving better play to the communication value of the reports.

Suggestion 4: Closely follow the trend, pay attention to the development and changes of core ESG issues such as environment and society under the new situation, and promote CSR information disclosure to be more contemporary.

Suggestion 5: Call on all parties to accelerate the application of a series of national standards on social responsibility through policy guidance, capacity building and performance evaluation, to jointly promote the improvement of CSR disclosure in China.

Based on GoldenBee CSR Report Assessment System 2021 (GBEE-CRAS2021), 1,802 Chinese CSR reports released by companies in China from January 1 to October 31, 2021 are collected and assessed in this Index Report, the 13th CSR Index Report released by the GoldenBee Research Team.

According to Guan Zhuxun, Executive Vice President and Chief Operating Officer of GoldenBee Consulting, the GoldenBee "Three Excellence" theoretical model of CSR reporting, namely excellent basic information disclosure, excellent response to core content, and excellent compliance with basic principles, was applied in the Index Report. GoldenBee profoundly analyzed the characteristics of CSR reports released in China, and offered suggestions on the CSR reporting in China to provide reference for enterprises.

Our findings

Characteristics 1:In 2021, the report quality reached an all-time high, and the comprehensive index reached 1,384 points, with a year-on-year increase of 6%. The proportion of reports in the development, good, and excellent stages increased year on year, the proportion of reports in the catch-up stage increased greatly, and those in the starting stage have decreased significantly. It is predicted that China's CSR report quality will advance to new levels during the 14th Five-year Plan period.Characteristics 3: The disclosure on corporate strategy and governance has seen a significant improvement, and information about top leadership's participation in social responsibility management has greatly increased. This year, the disclosure rate of different indicators of corporate strategy and governance has increased significantly year on year. Nearly 60% of the companies disclosed their CSR vision and strategy in their reports, and about 40% of them disclosed their social responsibility management framework in the reports.

Characteristics 4: The reports focus more on the performance of responsibilities to stakeholders, seeing a rising response to the expectations and demands of stakeholders. In 2021, the score rate of reports on the "communication channels and methods with stakeholders" and "clear and intensive explanation on stakeholders have increased significantly year on year, reaching nearly 60% respectively. A deeper analysis revealed that the information disclosure of key stakeholders such as employees, communities, customers, environment, and suppliers has expanded from CSR practices to the CSR concepts, requirements and expectations, communication channels and methods, and performance disclosures.

Characteristics 5: The reports disclose more information on fulfillment of responsibility to stakeholders, such as customers, environment, suppliers, communities, with higher disclosure rate of key topics such as customer privacy protection, pollution reduction and emission reduction, procurement principles, community voluntary activities, donation and disaster relief.

Characteristics 7: The quality of reports in financial and insurance industry and information technology industry has improved significantly. The index of production and supply industries of electricity, coal, water and gas has always been at a high level, and the report quality of transportation, warehousing and real estate industries has decreased. In 2021, the report quality of the social service industry has surpassed the transportation and warehousing industries, becoming the best for the first time. Compared with the base period, the index of ICT industry increased by 60.01%; the index of the financial and insurance industries has continuously improved for three years, seeing an increase of 23.87%; the index of production and supply industries of electricity, coal, water and gas increased by 31.59%.

Characteristics 8: The gap between the report quality of enterprises of different ownership has been further narrowed. The report quality of state-owned holding enterprises and private enterprises has increased significantly year on year. In the past three years, the quality of reports from central SOEs has always maintained at a relatively high level, which is much higher than that of other types of enterprises.

Characteristics 9: The report quality of mainland companies listed on SSE and SZSE has significantly improved year on year, and the gap between the report quality of mainland companies listed on SSE and SZSE and that listed in Hong Kong has narrowed. Since 2018, the mandatory implementation of the ESG Reporting Guide of the HKEX has promoted the report quality of mainland companies listed on the HKEX.

Our suggestions

Suggestion 1: Seize the opportunities and momentum to strengthen the understanding and action that make social responsibility help enterprises develop with high quality, and promote the quality of CSR report to a new level during the 14th Five-year Plan period.Suggestion 2: Guided by strategies and the concept of stakeholders, to strengthen the disclosure of CSR strategy, governance and management.

Suggestion 3: Be problem-oriented and focus on the expectations and demands of stakeholders, making up for the shortcomings of reports in normality and materiality, and giving better play to the communication value of the reports.

Suggestion 4: Closely follow the trend, pay attention to the development and changes of core ESG issues such as environment and society under the new situation, and promote CSR information disclosure to be more contemporary.

Suggestion 5: Call on all parties to accelerate the application of a series of national standards on social responsibility through policy guidance, capacity building and performance evaluation, to jointly promote the improvement of CSR disclosure in China.

Best Practices

- The 100-year brand — Air Liquide also has a sense of juvenile

- Beijing Public Transportation Corporation: Developing green transportation to build a harmonious and livable capital

- CGN: Building a modern factory in barren deserts and developing a new win-win cooperation model along “Belt and Road”

Upcoming Event

All the materials on the site “Source: XXX (not from this site)” have been reprinted from other media. They do not imply the agreement by the site.

All the materials with “Source: CSR-China Website” are the copyright of CSR-China Website. None of them may be used in any form or by any means without permission from CSR-China Website.

GoldenBee Official WeChat

Copyright © Csr-china.net All Right Reserved.

京ICP备19010813号